Americans' surge in refinancing interest reveals growing concerns

Americans' surge in refinancing interest reveals growing concerns

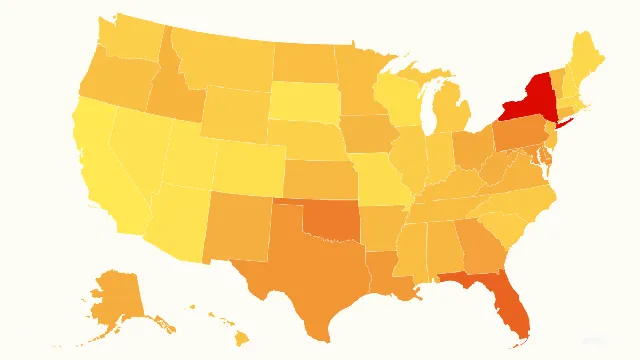

- Average closing costs for refinancing amount to $2,207, or 0.67 percent of the refinance loan amount.

- New York has the highest refinance closing costs in the U.S. at 2.06 percent.

- Rising mortgage rates and high closing costs may limit refinancing options for homeowners.

Story

In the months leading up to the start of the Iran war, Americans showed an increased interest in refinancing their mortgages. This trend was largely driven by a notable decline in mortgage rates that provided homeowners with an opportunity to improve affordability by restructuring their loans. However, the situation changed with the onset of military actions involving the United States and Israel. The subsequent joint strikes on Iran notably caused mortgage rates to rise above the critical 6 percent mark, ultimately influencing refinancing activities among homeowners. According to recent data compiled by Haver Analytics, applications for loan refinancing experienced a 4.4 percent decline in the week ending May 8 compared to the previous week, which highlights the volatility of the mortgage market in light of current events. Despite this week's dip, there was still a significant year-over-year increase of 14.9 percent in refinancing applications, indicating that many homeowners are still exploring options to enhance their financial situations. The average total closing costs for refinancing, which include recording fees and taxes, were reported at $2,207 or 0.67 percent of the refinance loan amount. However, these costs can vary significantly by state, making refinancing less convenient for homeowners in areas with higher fees. New York led the nation with the highest closing costs as a percentage of the sale price, totaling 2.06 percent. This was followed by Florida (1.36 percent), Oklahoma (1.13 percent), Pennsylvania (1.01 percent), and Texas (0.96 percent). The data suggest a correlation between higher closing costs and the states' respective mortgage taxes, underscoring the financial burden that many homeowners face when refinancing their loans. While refinancing can be beneficial for many, experts caution homeowners to be wary of rising mortgage rates, which might negate some benefits. Financial advisors, like Kyle Bass from Refi.com, suggest that considering alternatives such as Home Equity Lines of Credit (HELOCs) may also be worthwhile, particularly for homeowners who secured low mortgage rates in the past and wish to maintain them while accessing equity.

Context

The impact of the Iran War on mortgage rates is a complex issue that intertwines various economic and geopolitical factors. As conflict arises, especially in regions with significant oil production like Iran, the global oil prices often react strongly. An increase in oil prices typically leads to higher inflation rates, which can compel the central banks in various countries, including the U.S. Federal Reserve, to raise interest rates to combat inflation. Consequently, a rise in interest rates would directly affect mortgage rates, making borrowing more expensive for consumers. This is crucial as mortgage rates are often reflective of the broader economic conditions influenced by geopolitical tensions. Therefore, as the Iran War escalates, mortgage rates may inevitably rise, impacting the housing market and broader economy as potential homebuyers face increased costs of financing their homes. Moreover, the housing market is sensitive to changes in economic outlooks brought about by conflict. If the war creates a sense of uncertainty in the economy, potential homebuyers may delay their purchasing decisions, leading to lower demand in the housing market. This decrease in demand can generate downward pressure on home prices, which may offset the effects of rising mortgage rates. However, in a scenario where home prices drop significantly, the overall attractiveness of investing in real estate might still falter as consumers anticipate further declines, thereby inhibiting market recovery. Additionally, a war in Iran could lead to increased government spending on military operations, potentially diverting funds from critical domestic investments. This could stagnate economic growth, further complicating decisions made by the Federal Reserve regarding interest rates. The interplay between military expenditure and interest rates is significant; prolonged military engagements could prompt sustained budget deficits, creating pressure on government debt levels and influencing investor confidence in long-term economic stability. As interest rates rise, the cost of financing a home through a mortgage increases, leading to a prolonged period of uncertainty in the real estate market. In conclusion, the implications of the Iran War on mortgage rates are deeply interlinked with macroeconomic conditions, inflationary pressures, and shifts in consumer behavior resulting from heightened uncertainty. As the conflict evolves, it is critical to monitor oil prices, inflation rates, and economic growth indicators as they will provide insight into future mortgage rate trends. Understanding these dynamics is essential for both consumers in the housing market and policymakers seeking to implement measures to stabilize the economy in times of conflict.